Truckload spot rates are on track to rise more than 40% y/y in June 2026, net fuel. The US freight cycle has so far been supply-driven, but the freight demand outlook is supported by tight inventories, improving industrial activity, declining capacity, and falling tariffs, as discussed in the latest release of the Freight Forecast: Rate and Volume OUTLOOK report.

“Tighter supply remains the main reason for accelerating rates,” said Tim Denoyer, ACT Research’s Vice President and Senior Analyst. “As equipment investment declined and regulations fueled a driver shortage, the dislocation to an acutely tight TL market occurred fairly quickly this year. Most of this occurred before the May 14 Montgomery SCOTUS ruling, raising broker liability and further tightening capacity.”

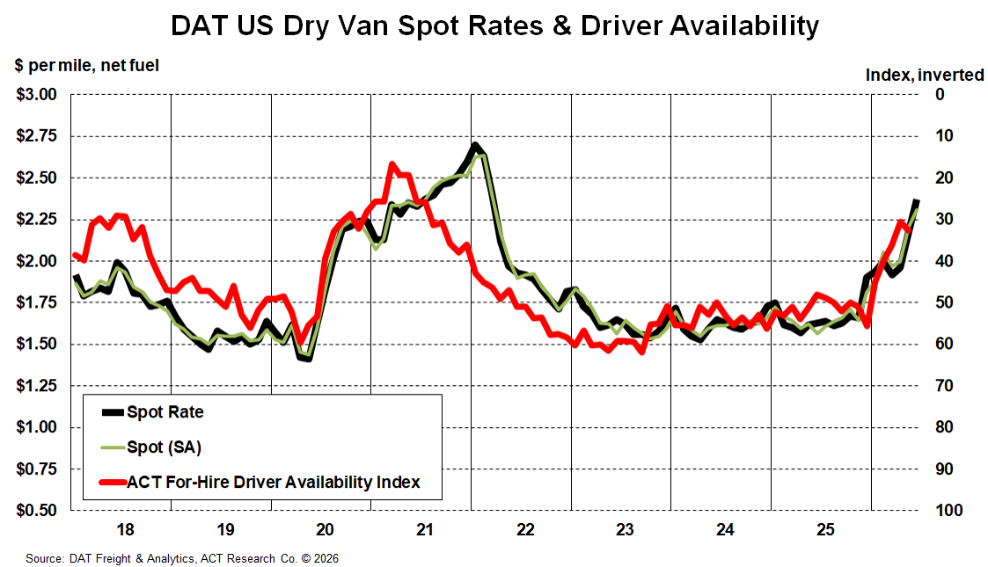

“The ACT Driver Availability Index remained in shortage territory in May at 32.6. While up from 31.5 in April, this survey-based diffusion index is neutral around 50 and acutely tight below 40. As seasonality softens after July 4th, some cooling off is likely, and load/truck trends have fallen from May to June, so the near-vertical trend is unlikely to persist. Net DOT operating authorities have improved a little in recent months in response to higher rates, and new Class 8 tractor sales are set to rise in 2H. But we think new regulations, including the MOTUS system requiring new USDOT numbers for all fleets from May onward, will continue to tighten capacity,” Denoyer concluded.

Freight Forecast Report Overview

The monthly 58-page ACT freight forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast provides unmatched detail on the freight rate outlook, helping companies across the supply chain plan with greater visibility and less uncertainty.

ACT Research Overview

ACT Research is recognized as the leading publisher of commercial vehicle truck, trailer, and bus industry data, market analysis and forecasts for the North America and China markets. ACT’s analytical services are used by all major North American truck and trailer manufacturers and their suppliers, as well as banking and investment companies. ACT Research is a contributor to the Blue Chip Economic Indicators and a member of the Wall Street Journal Economic Forecast Panel. ACT Research executives have received peer recognition, including election to the Board of Directors of the National Association for Business Economics, appointment as Consulting Economist to the National Private Truck Council, and the Lawrence R. Klein Award for Blue Chip Economic Indicators’ Most Accurate Economic Forecast over a four-year period. ACT Research senior staff members have earned accolades including Chicago Federal Reserve Automotive Outlook Symposium Best Overall Forecast, Wall Street Journal Top Economic Outlook, and USA Today Top 10 Economic Forecasters. More information can be found at www.actresearch.net.

Additional Resources

A supply-driven freight cycle doesn’t imply strong volumes, and this time is no different. The current 30% y/y increase in truckload spot rates, net fuel, coming out of Roadcheck, is driven primarily by tighter capacity, as discussed in the latest release of the Freight Forecast: Rate and Volume OUTLOOK report.

“Improving survey data, including a jump in the ACT For-Hire Volume Index, suggest our friends at medium and large dry van and reefer fleets are beginning to see significantly stronger demand, even as the broader market does not,” said Tim Denoyer, ACT Research’s Vice President and Senior Analyst. “The source of this early demand increase is primarily capacity reduction, which has accelerated this year due to an incipient driver shortage.”

“While the goods economy is providing little lift, the key question becomes, how bad will the driver situation get? In a word, worse. Truckload spot rates have risen materially in recent months as the ACT For-Hire Driver Availability Index has declined. This index was above 50, meaning a surfeit, rather than a shortage, from June 2022 to December 2025, 43 straight months. It fell to 30.4 in April. New FMCSA regulations have acted as a catalyst, and seem likely to result in tighter capacity and higher rates from here,” Denoyer concluded.

Click here to learn more information about ACT's most subscribed report.

ACT Research is featured regularly by major news outlets for our work covering Class 8 truck orders, sales, forecasting, used truck sales, freight rates, trailer sales, and much more. Get more trends, HERE.